COVID-19 & business FAQs

Melanie Richardson

16/06/2020

Up to date as of (15th June 2020)

We have had a number of enquiries over the past few months so we thought we would gather together our answers into an FAQs resource. If you have an urgent query or are in need of any advice at this time – please contact your Swindells’ partner using our contact details that can be found here: CONTACT DETAILS

What schemes am I eligible for as a self employed worker?

As a self employed worker or sole trader, there are a number of government schemes that you may be eligible for set up to help those whose livelihoods have been affected by Covid19:

Self employed income support scheme (SEISS)

The SEISS is a government scheme that provides eligible self-employed workers with a taxable grant to help with their financial situation.

The scheme currently allows you to claim a taxable grant worth 80% of your average monthly trading profits, paid out in a single instalment covering 3 months’ worth of profits, and capped at £7,500 in total.

If you’re eligible and your business has been adversely affected, you must make your claim for the first grant on or before 13 July 2020.

This scheme is being extended. If you’re eligible for the second and final grant, and your business has been adversely affected on or after 14 July 2020 you’ll be able to make a claim in August 2020. You can claim for the second grant even if you did not make a claim for the first grant.

Who is eligible?

You can claim if you’re a self employed individual or a member of a partnership and all of the following apply:

- you traded in the tax year 2018 to 2019 and submitted your tax return on or before 23 April 2020 for that year

- you traded in the tax year 2019 to 2020

- you intend to continue to trade in the tax year 2020 to 2021

- you carry on a trade which has been adversely affected by coronavirus

Your business could be adversely affected by coronavirus if, for example:

- you’re unable to work because you:

- are shielding

- are self-isolating

- are on sick leave because of coronavirus

- have caring responsibilities because of coronavirus

- you’ve had to scale down or temporarily stop trading because:

- your supply chain has been interrupted

- you have fewer or no customers or clients

- your staff are unable to come in to work

How to claim

In order to make a claim you must first check your eligibility and then have the following information to hand if you are eligible;

- Unique Taxpayer Reference (UTR)

- National Insurance number

- Government Gateway user ID and password

- UK bank details (only provide bank account details where a BACS payment can be accepted) including:

- bank account number

- sort code

- name on the account

- your address linked to your bank account

Follow the link below to check your eligibility and make your claim

https://www.gov.uk/guidance/claim-a-grant-through-the-self-employment-income-support-scheme

For the most up to date information please visit

Universal Credit

Universal Credit can help you with your living costs if you’re on low income or out of work. If you are not eligible for the SEISS you may be eligible for the Universal Credit scheme.

You may be able to apply for Universal Credit if:

- you’re on a low income or out of work

- you’re 18 or over (there are some exceptions if you’re 16 to 17)

- you’re under State Pension age(or your partner is)

- you and your partner have £16,000 or less in savings between you

- you live in the UK

Follow the link below to find out if you are eligible and to make your claim https://www.gov.uk/how-to-claim-universal-credit

Deferred tax payments

The government has put in place options to defer July income tax payments on account and VAT payments.

VAT payments

If you choose to defer your VAT payment as a result of coronavirus, you must pay the VAT due on or before 31 March 2021. If you defer a payment on account between 20 March 2020 and 30 June 2020 but the balancing payment is outside of these dates, the amount you must pay is the balancing payment less any deferred payments. Deferring payments will not create a repayment.

You can only defer:

- payments relating to the quarterly and monthly VAT return payments for the periods ending in February, March and April 2020

- payments on account due between 20 March 2020 and 30 June 2020

- annual accounting advance payments due between 20 March 2020 and 30 June 2020

The deferral does not cover payments for VAT MOSS or import VAT.

For the most up to date information please visit:

https://www.gov.uk/guidance/deferral-of-vat-payments-due-to-coronavirus-covid-19

Payments on account

You have the option to defer your July payment on account if you are:

- registered in the UK for tax and,

- are finding it difficult to make your payment on account by 31 July 2020, due to the impact of coronavirus

You do not need to tell HMRC that you’re deferring your payment on account. Choosing to defer will not stop you from being entitled to other coronavirus support that HMRC provides.

You must make your second payment on account on or before 31 January 2021 if you choose to defer. Other payments you may have to make by this date include any:

- balancing payment due for the 2019 to 2020 tax year

- first payment on account due for the 2020 to 2021 tax year

You can check payments you need to make towards your next tax bill by signing in to your online account.

For the most up to date information please visit

Mortgage support

The availability of a three month mortgage holiday was first announced in March and will come to an end in June. People who have taken advantage of this scheme will be contacted by their lender to discuss a way forward. Where consumers can afford to re start mortgage payments, it is in their best interests to do so. However, if people are still struggling and need help, a full extension of the mortgage holiday for a further three months until the 31st of October will be available as one of the options open to them.

To apply for the mortgage support, contact your lender and tell them you are experiencing payment difficulties due to coronavirus. There will be a fast track approval process in place and you won’t need to provide evidence or have an affordability test so you should get a quick decision.

Lenders have dedicated pages on their sites with an FAQ on how to apply and the terms of the application.

NB - Be aware even though credit scores will not be directly impacted, lenders may be able to determine whether someone has taken a payment holiday and use that information when assessing a credit application.

What schemes am I eligible for as a business?

BounceBack Loan Scheme (BBLS)

The Bounce Back Loan Scheme (BBLS) provides financial support to businesses across the UK that are losing revenue and seeing their cashflow disrupted as a result of the COVID19 outbreak and that can benefit from £50,000 or less in finance.

BBLS is available through a range of British Business Bank accredited lenders and partners, listed on the British Business Bank website https://www.british-business-bank.co.uk/ourpartners/coronavirus-business-interruption-loan-schemes/bounce-back-loans/current-accredited-lenders-and-partners/

A lender can provide a six year term loan from £2,000 up to 25% of a business’ turnover. The maximum loan amount is £50,000.

The scheme gives the lender a full (100%) government-backed guarantee against the outstanding balance of the facility (both capital and interest).

Who is eligible?

Your business must be able to self declare to the lender that it:

- has been impacted by the coronavirus (COVID19) pandemic

- was not a business in difficulty at 31 December 2019 (if it was, you must confirm your business complies with additional state aid restrictions under de minimis state aid rules)

- is engaged in trading or commercial activity in the UK and was established by 1 March 2020

- is not using the Coronavirus Business Interruption Loan Scheme (CBILS), the Coronavirus Large Business Interruption Loan Scheme (CLBILS) or the Bank of England’s COVID Corporate Financing Facility Scheme (CCFF), unless the Bounce Back Loan will refinance the whole of the CBILS, CLBILS or CCFF facility

- is not in bankruptcy or liquidation at the time it submits its application for finance

- derives more than 50% of its income from its trading activity (this requirement does not apply to charities or further education colleges)

- is not in a restricted sector (see link below for more information)

How to apply

To start your application please visit the link to find and approach a lender

For the latest up to date information please visit

Coronavirus Business Interruption Loan Scheme (CBILS)

The Coronavirus Business Interruption Loan Scheme (CBILS) provides financial support to smaller businesses (SMEs) across the UK that are losing revenue, and seeing their cashflow disrupted, as a result of the COVID19 outbreak.

CBILS has been significantly expanded along with changes to the scheme’s features and eligibility criteria. The changes mean smaller businesses across the UK impacted by the coronavirus crisis can access funding.

Importantly, access to the scheme has been opened up to those smaller businesses that would have previously met the requirements for a commercial facility but would not have been eligible for CBILS. Insufficient security is no longer a condition to access the scheme.

Your business must:

- be UK based in its business activity

- have an annual turnover of no more than £45 million

- have a borrowing proposal which the lender would consider viable, were it not for the current pandemic

- self certify that it has been adversely impacted by the coronavirus (COVID-19)

- Not have been classed as a “business in difficulty”on 31 December 2019 if applying to borrow £30,000 or more

Lenders will need further information to confirm eligibility. All lending decisions remain fully delegated to the 40+ accredited lenders. Up to date list of lenders

How it works

British Business Bank operates CBILS via its accredited lenders. There are over 40 of these lenders currently working to provide finance.

They include:

- high-street banks

- challenger banks

- asset based lenders

- smaller specialist local lenders

A lender can provide up to £5 million in the form of:

- term loans

- overdrafts

- invoice finance

- asset finance

For the latest up to date information please visit

Coronavirus Job Retention Scheme (CJRS)

The CJRS or Coronavirus Job Retention Scheme set up by the government in April has evolved over its lifetime.

From 1 July employers can bring furloughed employees back to work for any amount of time and any work pattern, while still being able to claim the grant for the hours not worked. From this date, only employees that you have successfully claimed a previous grant for, will be eligible for more grants under the scheme.

This means they must have previously been furloughed for at least 3 consecutive weeks taking place any time between 1 March and 30 June 2020. For the minimum 3 consecutive week period to be completed by 30 June, the last day an employee could have started furlough for the first time was 10 June.

This may differ if you have an employee returning from statutory parental leave

- Throughout June and July, the government will continue to cover 80% of furloughed employees’ wages up to a cap of £2,500. From August, the government payments will be the same as before, but employers must cover National Insurance and pension contributions.

- From September, the government’s contribution to wages will fall to 70%, with a cap of £2,187.50, while employers must continue to pay NICs and pension contributions, as well as 10% of wages up to the £2,500 cap.

- In October this falls to 60% of wages, with the employer increasing its payment to 20%, alongside NICs and pension payments.

How to claim

The first time you will be able to make claims for days in July, will be 1 July. You cannot claim for periods in July before this point. July 31 is the last day that you can submit claims for periods ending on or before 30 June.

If we act as an agent for your PAYE please contact us and we will be able to help you navigate the scheme.

If you are claiming yourself:

Please follow the link below which will take you through the process step by step

https://www.gov.uk/guidance/claim-for-wages-through-the-coronavirus-job-retention-scheme

For the most up to date information and guidance on the CJRS please visit this link

https://www.gov.uk/guidance/claim-for-wage-costs-through-the-coronavirus-job-retention-scheme

Statutory Sick Pay

The Coronavirus Statutory Sick Pay Rebate Scheme will repay employers the Statutory Sick Pay paid to current or former employees who are eligible for sick pay due to coronavirus. As yet there is no end date to the scheme.

Who can use the scheme?

You can use the scheme as an employer if:

- you’re claiming for an employee who is eligible for sick pay due to coronavirus

- you have a PAYE payroll scheme that was created and started on or before 28 February 2020

- you had fewer than 250 employees on 28 February 2020 across all your PAYE payroll schemes

Employees do not have to give you a doctor’s note for you to make a claim, but you can ask them to give you either:

- an isolation note from NHS 111 - if they are self isolating and cannot work because of coronavirus (COVID-19)

- the NHS or GP letter telling them to stay at home for at least 12 weeks because they’re at high risk of severe illness from coronavirus

The scheme covers all types of employment contracts, including:

- full time employees

- part time employees

- employees on agency contracts

- employees on flexible or zero hour contracts

- fixed term contracts (until the date their contract ends)

Follow the link below for information on how to claim https://www.gov.uk/guidance/claim-back-statutory-sick-pay-paid-to-employees-due-to-coronavirus-covid-19

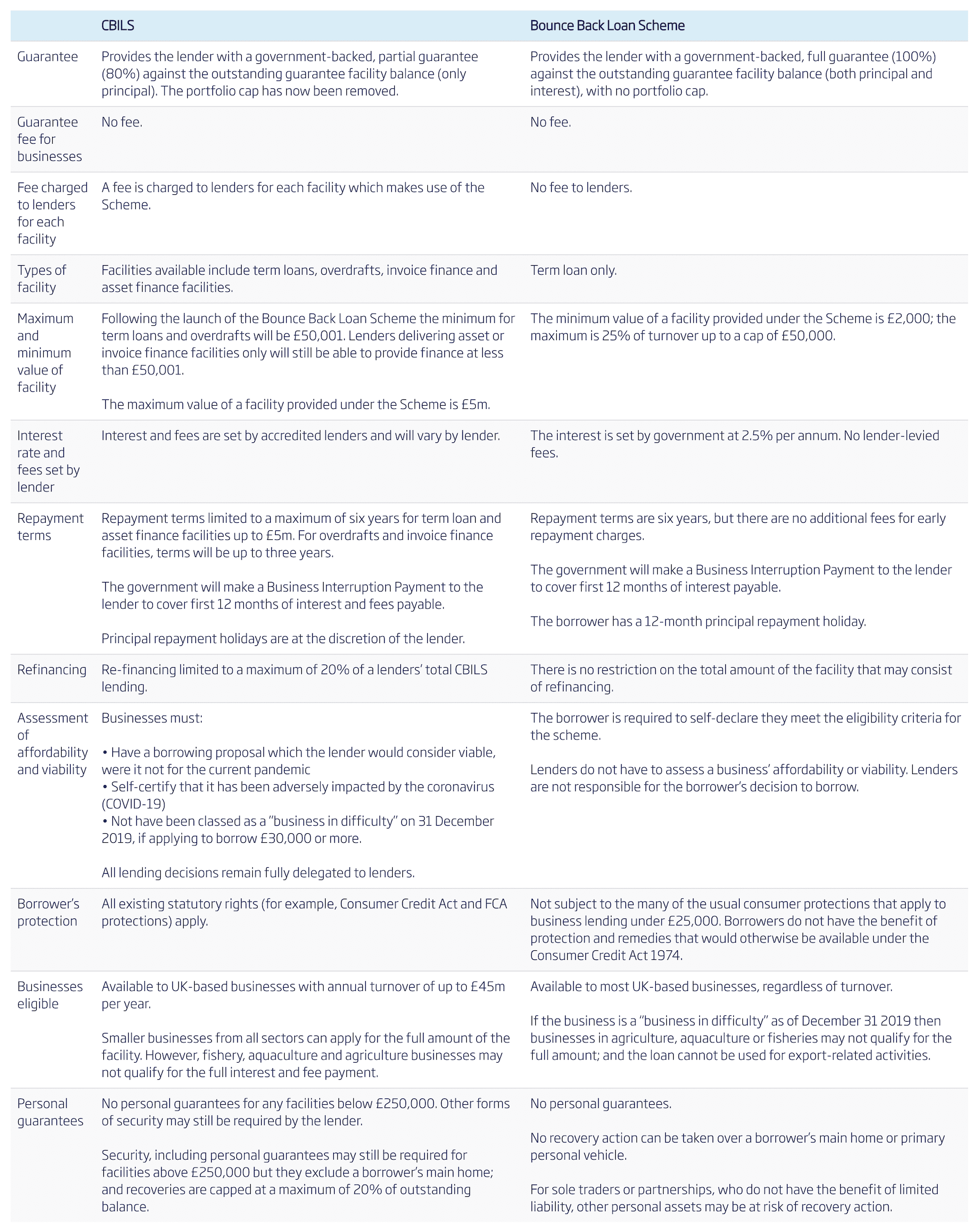

What’s the difference between CBILS and the BounceBack loan?

Speed, eligibility & assessment criteria:

Speed is one of the main benefits of the BounceBack loan scheme. Finance is reaching businesses within a day or so of applications being filed if accepted. However it has a cap of £50,000 or 25% of your turnover whereas the CBILS maximum loan is £5m. It is also only available to businesses with an annual turnover of under £45m. The criteria for acceptance also varies where you can self-certify for the BounceBack loan the CBILS requires a more stringent checking process from lenders.

For more detailed information please see the table below.

Source:

I’ve furloughed people, but we are running out of work – I need to make people redundant. How do I do that?

We can’t advise businesses on how to make their staff redundant. There are legal processes that must be followed to ensure that you protect yourself and your employee.

Croner provides a free advice line to businesses https://enquire.croner.co.uk/redundancy/

There is also a government webite which might be of use https://www.gov.uk/staff-redundant

Before you do anything, you should speak to your legal or HR advisor, who will be able to address your specific situation and advise accordingly. There are other options to redundancy and these may suit your situation better.

What do I do if I think my business is going to fail?

The first thing that you should do is call your Swindells partner to discuss your situation. We have a vast amount of experience in helping businesses through difficult times and will be able to provide advice. It may not be as bad as you think. If your business has reached a critical point there are number of actions you might be able to take:

- talk to your creditors and try to agree terms, especially HMRC

- get a time to pay arrangement in place to pay down debt over time

- refinance if your current lender has onerous repayments

- talk to insolvency practitioners about a possible mechanism that can save the business

If you have any further questions that you’d like us to help you with, please get in touch with your Swindells’ partner contact details that can be found on our website here:

Sign up to receive our private content

straight to your inbox

KEEP UP TO DATE

We use social media to deliver our updates to you on the go, wherever you are. We only post relevant content that will help you run your business.